Morgan Housel’s ‘The Psychology of Money’ forces you to take another look at personal finance, investing, and business success through the lens of psychology and behaviour. These fields of study have their roots in math, data, and calculations. However, in this book, Housel highlights how everything, from your personal history and experience to your unique world view, ego, pride, marketing, and odd incentives work together to help you finally form a financial decision.

Key Takeaways

When it comes to earning money and building wealth, it really doesn’t matter how smart you are. Instead, what really matters is how you behave.

Even the smartest people can lose control of their emotions and plunge into financial disasters while ordinary people with no financial education, but robust behavioural skills, can become wealthy.

It is not enough just to know how to do something. You must be able to fight with internal emotional and mental turmoil in order to make the best financial decisions.

Considering the lack of accumulated wisdom in terms of modern finance, many of the poor financial decisions that you end up making arise from peoples’ collective inexperience.

You must not risk what you already have and require for things which you do not have and do not actually need.

Creating wealth and maintaining wealth are two different things. Creating wealth is easy, but keeping it is very difficult.

While there are many ways to accumulate wealth, there is only one way to maintain it, and that involves being frugal and paranoid of potential losses.

Experience can be a boon and a bane

“Your personal experiences with money make up maybe 0.00000000001% of what’s happened in the world, but maybe 80% of how you think the world works.”

Stop the goalpost from moving

You should know when you have enough wealth and then stop wanting more. Throughout history, greed or a craving for ‘more’ has been the downfall of many of the rich and famous. When you keep running after more, you inevitably start taking more risk than you should. Know when to stop. Good investing is not about earning the highest returns. Instead, it is about making good enough returns for the longest period of time. Compounding is the way to create long-term wealth.

Savings is the dealmaker

The rate at which you save is far more important than your income or your investment returns. Generally, beyond a certain income level, you will find three types of people. First are the people who save. Second are the people who don’t think that they earn enough to save. And, third are the people who think that they don’t need to save. However, over a longer period of time, it will be the people belonging to the first category who will end up successfully creating and maintaining their wealth.

Leave a room for error

When you are investing, always remember that you are dealing with probabilities and not certainties. Thus, you should always leave a room for error, the best way of doing this is by avoiding single points of failure and spreading your investments. It is also a great idea to always have a good emergency fund.

Eight Fixed Income Instruments that beat the best FD Rates in India

The alternatives we will discuss are categorized into three risk buckets.

No-Risk

Lower or equal risk to FDs

Higher Risk than FDs

Risk category: No-Risk / Sovereign Risk

This is the list of alternatives where you can invest for better returns without taking any additional risk than Fixed Deposits. For that matter, these are way safer than any bank’s FD. Because you are lending money to the Government, they have a sovereign rating.

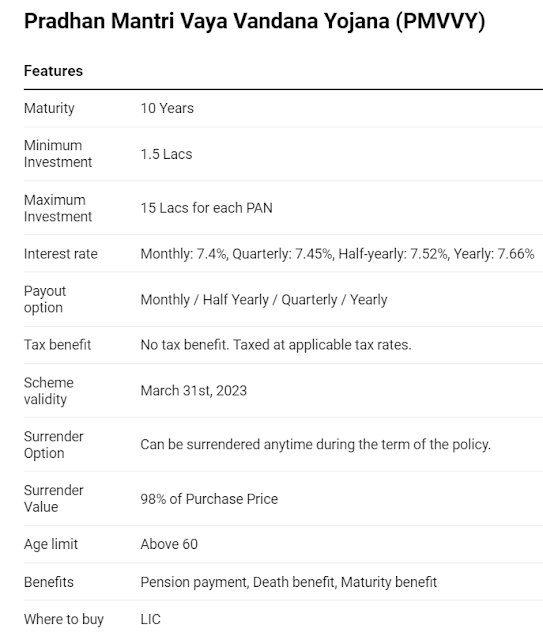

1. PMVVY Scheme

PMVVY is a government-subsidized pension scheme for senior citizens. It currently provides an assured return of 7.66% pa. The interest rates vary according to interest payouts (Yearly, Half Yearly, Quarterly, or Monthly).

The minimum purchase amount is 1.56L & maximum is 15L. You can lock the high-interest rate for ten years. There is no tax benefit for the scheme. The individuals are taxed at applicable rates, and TDS is not deducted. You can invest in PMVVY via LIC India.

2. Senior Citizens Savings Scheme

It is a government-backed savings scheme that was launched in 2004. The primary objective is to enable senior citizens to ensure a regular flow of income.

As the name suggests, it is only eligible for senior citizens. The interest rate has been set as 7.4% pa as of today. The minimum investment is 1000 & the maximum investment is 15 Lacs per individual. Interest payout is every quarter.

Maturity tenure is for five years with a one-time option to extend for three more years. So, in total, it will be eight years. You can invest in this scheme from any authorized bank or post office.

3. RBI Floating Rate Bonds

RBI has launched a floating rate savings scheme in July 2020, which has a maturity of 7 years. The interest on the bond is linked to National Savings Certificate. It offers an NSC + 0.35% rate of return.

The current interest rate of NSC is 6.8%, and you add 0.35% to it. So RBI Floating bonds will give a 7.15% interest per annum. You can invest in RBI Bonds from select banks like HDFC Bank, Axis Bank etc. or via brokers like ICICI Direct and HDFC Securities.

4. Government Securities

G-Secs are issued by the Government of India with various maturities (from 91 days to 40 years). The interest rate depends on maturity. The minimum investment is 10,000, and the maximum is 2 Cr per PAN. You can invest in G-Secs via the RBI Retail Direct platform or brokers like Zerodha.

Risk category: Low or equal risk as FDs

The below names will carry lower or, in some cases, equal risk when compared to Fixed Deposits. Some of these are bonds issued by Public sector companies. In adverse cases of stress, GoI will come to the rescue.

5. PSU Tax-Free Bonds

Major Public sector companies like PFC, HUDCO, NHAI, NTPC, NABARD, etc., had issued tax-free bonds from 2010 to 2015. These are traded in the secondary market and yield anywhere between 4.5% to 4.9% or higher.

They are AAA bonds & provide good liquidity. You can check with your broker/market maker for large quantities and get a better yield. Please note that you are not required to pay any tax on the interest received from these bonds, unlike others.

6. Savings account of Equitas and AU Small Finance Banks

Equitas Small Finance Bank offers a 7% interest rate on Savings accounts with a balance above 5L up to 2 Cr. Alternatively, you can also open a Niyo X (a Neo bank) account, which will open an Equitas bank account along with all the features of new-age banking.

Along similar lines, AU Small Finance Bank is also offering a 7% interest rate on Savings accounts with a balance above 25L up to 1 Cr.

But how safe are these Small Finance Banks? Before that, let’s try to understand DICGC.

Deposit Insurance and Credit Guarantee Corporation is a wholly-owned subsidiary of RBI. It provides insurance to the depositors up to a limit of 5 lakh per account holder per bank. It works as a protection cover for bank deposit holders when the bank fails to pay its depositors. Basically, it is like RBI saying to the depositors, ‘Hey, if shit hits the fan. We cover you up to 5 Lacs’. Both Equitas and AU bank are covered under DICGC.

Equitas Small Finance Bank interest rate

AU Bank interest rate

Risk category: Higher Risk than FDs

The names we are going to discuss bear some risk and can even lead to capital loss. You have to be very choosy here. There is no capital protection in this instrument. Please check with your financial advisor before investing in these instruments.

7. High rated Corporate Bonds

Many private companies and NBFCs will raise money from the markets by issuing Debentures, Commercial papers, etc. Based on the risk profile of the company, they trade anywhere between 6.5% to 8.5% or more, depending on the liquidity and financial situation of the company.

A word of caution:

Dealing with corporate bonds is tricky. The underlying company may look great from the outside. But the cockroaches can only be found if we look deeper. Debt markets are always a lead indicator for what the company is going through. If the bonds of a particular company are trading at an exorbitant yield, it would be better for retail investors to stay away from it.

8. INVITs and REITs

In recent times InvITs and REITs have gained popularity among investors. They offer retail investors the opportunity to invest in alternate asset classes like Real Estate, Power Plants, Roads, etc.

They are a mix of both Debt & Equity. The regularity of dividend payments gives it a touch of a debt instrument. At the same time, the unitholder participates in the company’s growth trajectory, much like an Equity investor.

There are 3 INVITs and 3 REITs listed in India. The Dividend Yield is in the range of 5.4% to 8.5% for different companies.

It is time to look for alternatives. At the same time, we shouldn’t compromise on RISK. These instruments provide you with:

Regular interest payments

Sovereign & PSU credit rating

Relatively better interest

Investments offering better returns than FDs

Data as of Apr 6th, 2022

PMVVY

Sovereign Risk

7.66%

10 years

Senior Citizens

G-Secs

Sovereign Risk

6% to 7.2%

3 months to 40 years

Everyone who is looking to have regular cash flows and build long term debt portfolio

RBI Bonds

Sovereign Risk

7.15%

7 years

Everyone who is looking to have regular cash flows and build long term debt portfolio

SCSS

Sovereign Risk

7.40%

8 years

Senior Citizens

PSU Tax Free Bonds

Low Risk

4% to 4.8%

depends on the bond

Everyone who is looking to build long term debt portfolio

Corporate Bonds

Some Risk

6% to 10%

depends on the company & the bond

Everyone who is looking to build long term debt portfolio

InvITs / REITs

Some Risk

5.2% to 8.4%

depends on the performance of investee companies

Everyone who has a higher risk appetite to invest in risky debt for better yields

Equitas SFB / AU Bank Savings account

Low Risk (up to 5 Lacs)

7%

No fixed tenure. However, the interest rate may change in the future.

Someone who wants to park t

This post is for informational purposes only. Before investing in any of the above mentioned products, check with your financial adviser about their suitability for your needs.